Electric Skies

There are hidden messages in the sky, if only we had the eyes to read them.

Up high, above the clouds and beyond most peoples’ awareness, the ionosphere blusters and boils with electric turbulence. It is the byproduct of our atmosphere shielding us from a constant siege of solar and cosmic radiation, which tears up air molecules and leaves a layer of electrons in its wake, sometimes visible as the aurora borealis. The ionosphere is defined as the layer of the atmosphere that has sufficient electric energy to affect the propagation of radio waves. Satellites call the ionosphere their home, as do weather balloons, the highest-flying jets, rockets to the stars, and ships to the edge of the atmosphere. Their operations are determined by the ionospheric environment, and they must coordinate their actions around the ionosphere in order to reliably carry out their mission. There is weather up there too, but instead of the familiar weather of moisture, temperature, and rainfall, ionospheric weather is made of ions, electrons, and insane bursts of energy that can explode metals. (Fortunately, we are shielded from most of those effects.)

You don’t have to be in the ionosphere to be affected by it. The scope of human activities that are directly affected by the everyday changes of the ionosphere is surprising to most. If you care about GPS guidance for your Uber driver or dating app, communication over satellite phone, listening to XM radio, and the location of the airplane that your relatives are riding to visit from another country, then you care about the ionosphere. All telecommunications on Earth either bounce against or shoot through the ionosphere.

These activities and more are all at the mercy of the ionosphere and can be totally cut off during an ionospheric storm. These storms feature severe electric turbulences which mix and jumble normal pathways of RF signals, preventing the radio signal beam from flying true, like a mirage does to light. Satellite GPS and communications cannot work when the signal is scrambled unrecognizably or lost completely. Military operations around positioning, navigation, and timing tend to be faster and have more accuracy problems than civilian needs, so the same turbulences that wouldn’t be noticeable for civilians have cost governments tens of millions of dollars.

Though so much human technology operates in the ionospheric context, it is the least known layer of our atmosphere. Whereas we can know the weather hour by hour right outside our door, for the ionosphere we can only know what the weather will tend to be this week somewhere above our country.

Humans did not have a good reason to understand the ionosphere until very recently. While weather was a primary determinant of human events like the World Series, D-Day, and a Saturday family picnic, the troubles from adverse ionospheric events had not been evident. You can still have a lovely day in complete ignorance of the ionospheric state above you. However, the more we integrate Wi-Fi, 5G, and satellite services into our lives, the more we will have our days ruined by a surprise in space weather.

But the methods for understanding the weather on the earth’s surface and the space weather in the ionosphere are fundamentally the same. For weather forecasting, doppler radars and other sensors collect weather data around the world, refine that data through algorithms, and present the current and forecasted data onto maps. For the areas without weather sensors, computers fill the gaps with best guesses, smoothing the gradations of temperature, humidity, and other building blocks of weather. For the ionosphere, there simply isn’t the same amount or quality of data. Further, the fundamental properties of the ionosphere are less well known, so the computers must make larger assumptions in resolving data gaps. Bigger holes, and worse tools to fill those holes.

This is the problem precursor-SPC is solving today. They are bringing computational rigor and hardware out to sense the ionosphere to shed real, operational light onto the ionosphere. precursor has developed a hardware ground station that measures the ionosphere to high sensitivity, and a proprietary AI algorithm that can combine, assimilate, and fill the holes between the sensors. The resulting ionospheric data is 1000x more accurate than the state of the art. Instead of knowing if it’s just a bad weather day, you can know that you should go outside at 4:00 pm with three layers of clothing and avoid Cincinnati. That amount of operational granularity is projected to save airlines millions in operational costs when flying over the north pole or in the arctic circle, save space and ground infrastructure operators a combined billions and improve the efficacy of military operations by an equivalent amount.

precursor’s representation of the ionosphere is in fact so high resolution, they have noticed patterns no one else has noticed before: a reliable causal relationship between certain ionospheric disturbances and future seismic events.

The electric nature of earthquakes isn’t completely unheard of; it is well known that the magnetic fields around Earth are in part due to our liquid mantle, otherwise known as a bunch of liquid rocks shooting off electric current and magnetic fields. Another known phenomenon is that rock, when under sufficiently high pressures, moves from acting as an insulator to a conductor of electricity. This seismic electricity shoots up and sends visible ripples through the ionosphere. Before, scientists could not distinguish if one particular perturbation came from solar or seismic activity. But now, with precursor, we can have the whole picture not be blurry for the first time and can characterize the difference in what solar activity disturbance is, and seismic activity disturbance.

Earthquakes grow and progress through a set of predictable steps, and precursor predicts earthquakes by characterizing the observed ionospheric turbulence equivalents of those same steps. These steps are the earthquake’s precursors from which the company derives its name. By and large, earthquakes result when tectonic plates grind against each other with localized high-pressure points. This visible observable seismic fact happens around 72 hours before the “snap” and must build up to sufficient strength before the snap happens and damage is done. From this, we see that with sufficiently high accuracy of the ionospheric model, you can know where, when, and how strong earthquakes are going to happen at least 72 hours in advance of the snap.

There are other entities that know how earthquakes happen, but their solutions are fundamentally different from what precursor does. The US Geological Survey can tell you when the earthquake’s echo will be, a few seconds to a minute after the initial quake. But little can be done in those few seconds to avoid critical damages at the event horizon. Others can tell you there will be a big earthquake in California sometime in the next 30 years — sort of obvious but not particularly useful other than for writing disaster movie scripts.

Preparedness is essential. Knowing how damaging earthquakes can be, and how much can be done to prepare for large seismic events 72 hours prior, the value of precursor is clear. The “big one” no longer has to be a complete surprise that can happen at any time. Now, we can shine a light on this terror, and be more aware of the world we live in.

The Unicorns Have Arrived

The age of billion-dollar aerospace startups is here.

Aerospace has long been one of the largest and most powerful global industries, comprised of space, aviation, and defense markets, and — until recently — the big names hadn’t changed much over the last fifty years. In the last 12 months, however, we’ve seen more than 20 aerospace startups evolve from “early-stage” to unicorns, through either direct listings, SPACs, or late-stage private funding rounds.

Following the first Uber Elevate summit four years ago in Dallas, we wrote an article for TechCrunch where we stated the next unicorn would come from the aerospace industry. At the time, only SpaceX and Planet had earned that title, but the writing was on the wall.

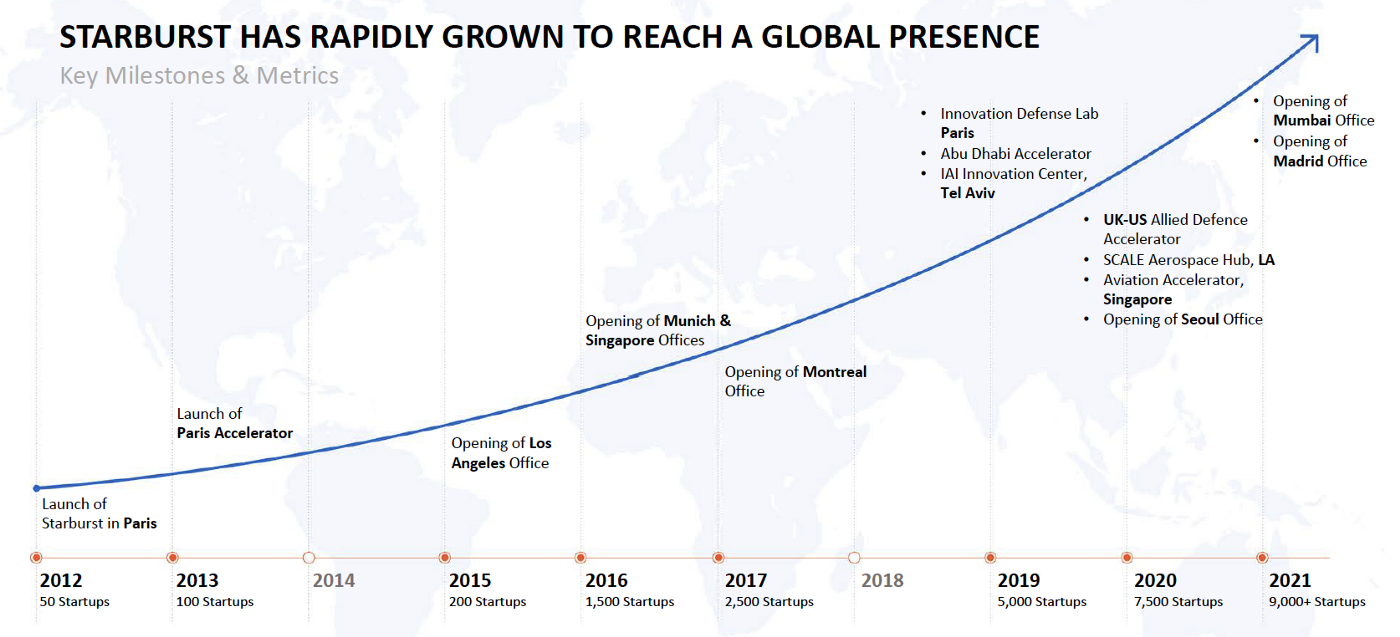

In the ten years since we founded Starburst, the world’s first and only global aerospace accelerator, we have gone from incremental to industry-disrupting change. Advances in manufacturing and computer processing have greatly decreased barriers to entry, agile startups have thrived in the competitive market, and investors are hungry to capitalize on this new global space race and the technology driving change across the transportation sector.

Cutting-edge, disruptive companies can now grow into successful commercial enterprises.

If we look back on the past year in more detail; more specifically the most recent three months, valuations of aviation, space, and defense companies have skyrocketed — literally.

There are several key takeaways from the growth we are witnessing:

Aerospace has become a very attractive market: for entrepreneurs and private investors.

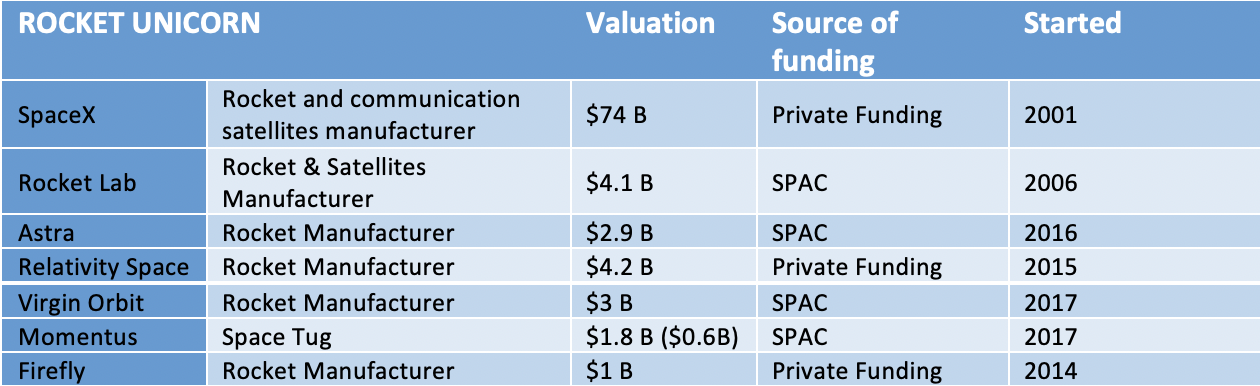

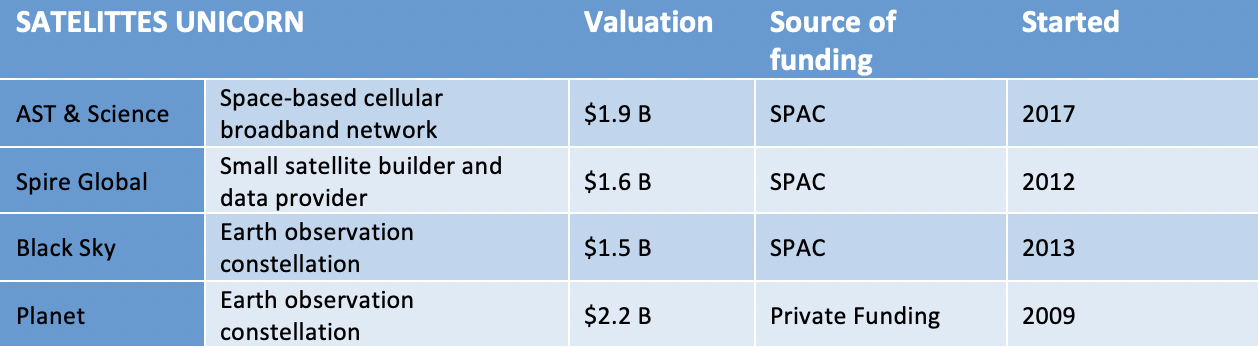

There are now more than 26* publicly traded, or soon to be in 2021, “startups” with a valuation over $1 billion each. These new players represent a combined total valuation close to $200B. Compared to Boeing’s market cap today which is roughly $130B and Airbus’ at $90B. SpaceX and Palantir make up a large portion of that $200B, but others can and will reach those numbers.

When we started Starburst, there were only a handful of new companies coming to life per year. Today, our team is scouting more than 3,000 new startups every year, predominately in the US, UK, and Israel, but also in countries like France, India, Singapore, Korea, and Japan, whose governments are increasingly investing in the sector.

Space is not only sexy but critical for understanding our own planet: we will continue to see successful tech entrepreneurs with deep pockets launching aerospace businesses.

Aviation is just as hot as the space sector.

Looking at the 26* startups mentioned below, 13 are connected closely to space, but 11 are classified as aviation companies. Though space startups tend to get stronger media coverage, aviation startups are just as hot, showing comparable funding and valuations.

Notably, the way we think about urban mobility and global transportation is changing and rapidly. Aviation is being fundamentally redefined by massive improvements in battery technology, electronics, and autonomy, as well as pressure to become carbon neutral. Evidenced by the major investments Toyota & Hyundai have made in electric vertical take-off and landing (eVTOL) aircraft, it’s likely that the future of cars is in the air.

Liquidity events are happening much faster.

SpaceX was founded roughly 20 years ago, and although still not a public company, private investors have been able to exit and see major profits. Planet started 10 years ago, and similar companies that have achieved $1B valuation were founded in the last five to eight (5–8) years. Relativity Space became a unicorn in four (4) years; Momentus (a Starburst portfolio company) had achieved unicorn status in less than 36 months (mindful there have been developments since).

The implications of this for the venture capital market are enormous. Startups once considered too risky or dismissed as science project investments have been shown to fit within a standard 10-year fund duration — and now even shorter!

Returns are much higher.

As valuations continue to soar, with companies like Virgin Galactic seeing valuations of not $1B but $8B, it is possible for early-stage investors to see returns on the order of 50–150x. Just one aerospace startup in your portfolio assures a return of your fund of at least 5x with liquidity even before the end of a 10-year fund duration.

At Starburst, three (3) portfolio companies will go public in 2021 alone, all achieving the $1B valuation mark, with liquidity in less than four (4) years.

This is just the beginning.

Rocket concepts are improving every month. Satellites are getting smarter, more economical, and development has been slashed from three years to one. Planes are moving faster, with lower emissions, and market pressures driving even Boeing and Airbus to rethink form and function. We will see hydrogen-based mobility companies, like our portfolio company ZeroAvia, join the unicorn club soon. Air taxis will become an integral part of urban mobility, like Craft Aerospace. Drones are delivering packages and heavy freight like Skyways.

This is the future today. The changes in aerospace are linked to developments and opportunities in energy, autonomous ground transportation, communication systems, AI, AR, manufacturing, new materials, and so much more. We are modernizing a global infrastructure and enabling the launch of more ambitious projects and a completely new set of technologies. Change is only going to accelerate and exponential growth in aerospace is now a given.

Here’s to the decade of innovation that we’ve been promised for decades…

* Of the 26 businesses captured in the table, two have undergone new valuations — Momentus at $566m, Archer at $1.7b, and

one has since folded its business— Aerion Supersonic.

Starburst Goes Lightspeed

The aerospace industry is at a pivotal point, and we at Starburst are marking this moment with a new look. This is our story–this is the industry’s story–and this is who we are today.

A Starburst is a galaxy undergoing an exceptionally high rate of star formation. This is analogous to the unprecedented amount of business creation the space and aviation industry is currently experiencing. Where there used to be a handful of new startups in aerospace every year, there are now thousands. We saw this potential when we formed our company; today the rate of technological innovation is ever-increasing, barriers to entry have lowered dramatically, and investors see incredible opportunity. We are at the center of all this, connecting entrepreneurs, researchers, investors, industry, and governments, catalyzing innovation across the ecosystem. We are Starburst.

When we started in 2012, we aimed to address a clear problem: the Aerospace & Defense industry wasn’t advancing at the rate technological and global development demanded. Historically funded by government only and very insular, there was an opportunity to shake up an industry. Our team has an extensive background consulting in A&D, so we began by coaching the largest players on how to engage and participate in the then-emerging culture of “open innovation.”

From the beginning, we went to where the innovation was happening. Our knowledge of emerging technologies and trends made us trusted advisors, and we quickly grew to work with 50+ corporations around the world, tackling critical challenges surrounding their growth and investment strategies. Our knowledge of new players in the sector made us invaluable in due diligence for M&A, understanding the competitive landscape for new technology, or crafting a go-to-market strategy for a new product.

We have completed 75+ consulting studies to date across mobility, communications, and intelligence.

And the number of startups in the sector has grown every year. The landscape changed with extraordinary advances in computation and manufacturing, a second global space race, and private company potential. We saw the value we could bring to the industry by supporting startups as well as our corporate clients.

In 2015 we launched Starburst Accelerator.

The first and only global aerospace-focused startup accelerator program in the world, we built Starburst Accelerator to help speed the entry of new technologies into the market. We started working with founders on a case-by-case basis to grow their businesses; working with them for a full year, helping them to raise capital, hit critical growth milestones, and secure industry traction. Connecting visionary founders in the Accelerator to our extensive network of global aviation, space, and defense leaders — fostered in the parallel consulting practice — was a force multiplier. This was a defining moment for Starburst, meeting a critical need and solidifying our role as the catalyst for innovation across the industry.

Today, we are witnessing industry disruption, and we see our success here: in the explosion of startups, in the over 25 aerospace unicorns operating today, in the increasing number of investors hungry to get involved in time. There has been a fundamental shift in how R&D is funded, how risk is factored in an increasingly competitive marketplace, and, as a result, product development has accelerated across the industry.

This is the future we worked to build.

Over the last 24 months, during a global pandemic, the Starburst team has doubled to 60 employees and added 4 new international offices. Everyone is noticing this boom of entrepreneurial talent, new business creation, and technology maturity: we’ve seen corporate and government interest exponentiate. This has brought us to another critical moment in our growth.

Over the last year, we’ve launched 5 new accelerator programs.

BLAST, SCALE, ASTRA, Allied Defense, and the Singapore Aviation Accelerator are just a taste of what’s to come.

We are building a one-of-a-kind global aerospace ecosystem, and we are focused on bringing new people, new ideas, and new possibilities into the industry. Our goal is to inspire a new generation of entrepreneurs and investors to pursue the advancement of novel technologies with aerospace applications, and we are supporting this next generation of startups from the ground up. And we can’t do it alone; we are collaborating with governments and industry leaders who want to help us shape the future.

And we are raising a fund, deepening our commitment to the technology the world needs.

Working with startups from ideation through the funding necessary to scale in a meaningful way, we are creating opportunities for commercial success in space, aviation, defense; we are supporting technologies that are changing infrastructure, energy, autonomous ground transportation, climate monitoring, communication systems, AI, AR, manufacturing, new materials, and so much more. We are expanding the understanding of and possibilities within the industry.

The new Starburst brand is a celebration of a decade of growth.

A Starburst is the hottest place in the Solar System. A Starburst is not just the center of new life but the center of opportunity. It is critical to get this re-brand right and articulate this powerful sentiment.

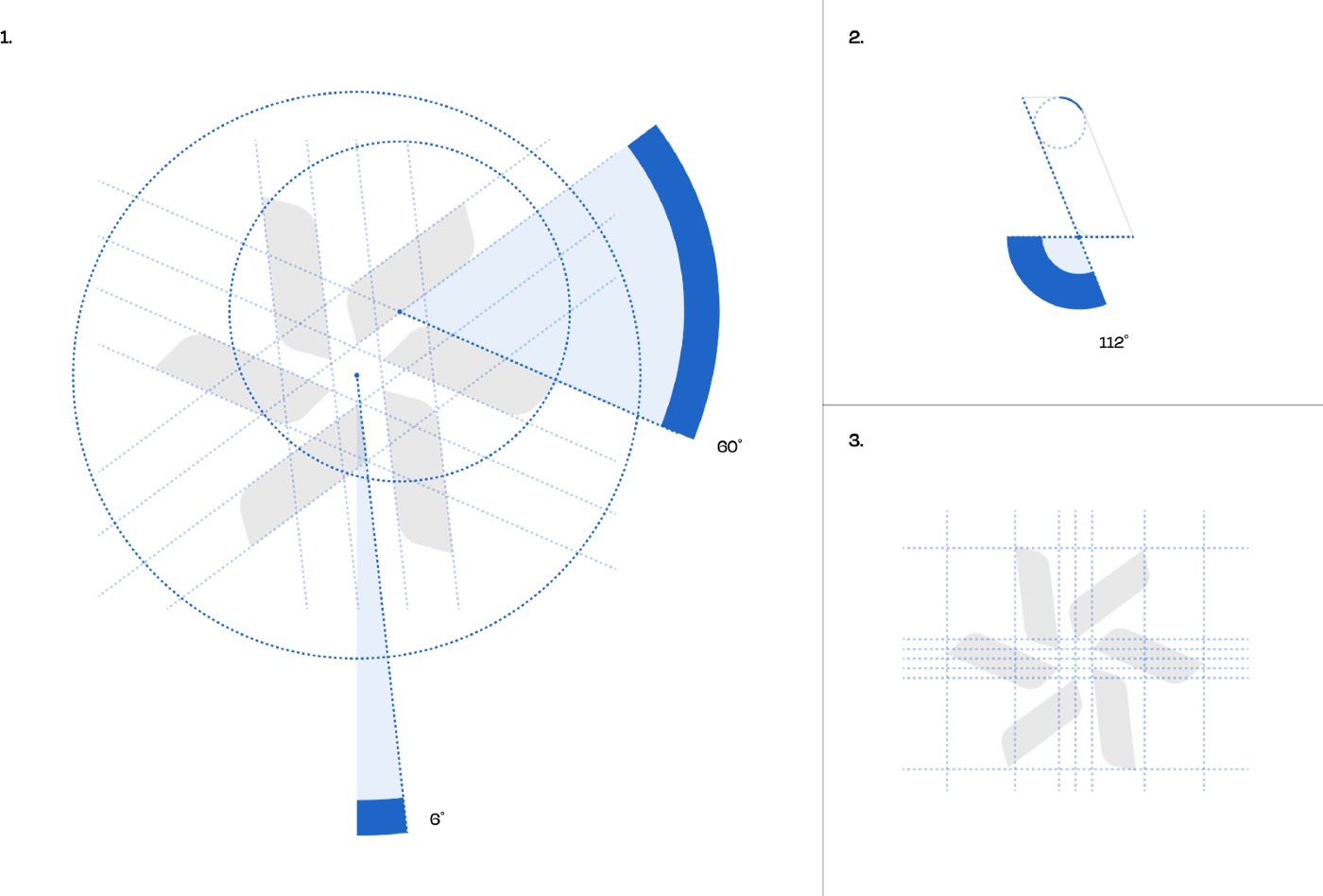

Two major themes define the logo redesign: the creation of new stars and the will to fly ever higher. Each block is in the shape of a winglet, spiraling together to achieve flight and propulsion. And the negative space between each winglet comes from the star itself — symbolizing the idea that you cannot have one without the other.

These themes tie into our story and the state of our industry. Our sector is overflowing with talent and passion and the support needed to pursue even greater opportunity; we take pride in the creation of new stars and their ability to radiate incredible energy and growth. And we will fly ever higher. Whether a member of the Starburst team, a portfolio company, or an investor in our network, we all have a penchant for flight. Wings and propulsion are the fundamentals for taking off and climbing high. At Starburst, it is our mission to propel businesses and accelerate their ascent to grow and compete.

Welcome to the new Starburst — a galaxy of exceptional energy giving flight to a growing industry, changing the way innovation happens in aviation, space and defense.

If you haven’t yet, we invite you to visit our new website (https://starburst.aero/), to reach out, to get involved. We are looking for entrepreneurs, investors, educators, corporate partners — we want to connect with all the brilliant human beings who are focused on building the future.